The global Fiberglass Reinforced Plastic (FRP) market is undergoing a period of sustained, accelerating growth that is reshaping the industrial materials landscape. Valued at approximately USD 72 billion in 2024, the composites industry is projected to reach USD 108 billion by 2030, growing at a Compound Annual Growth Rate (CAGR) of 7.2%. This trajectory is driven by a convergence of regulatory mandates, industrial decarbonization pressures, and a decisive technical shift away from traditional metals.

For manufacturers like Ghaziabad Polymers Pvt. Ltd. (GPPL), which has been operating in the FRP space for over three decades, this market expansion represents both validation of a long-held engineering philosophy and a significant opportunity to scale client solutions across new geographies and sectors.

Market Overview

FRP composites — encompassing glass fiber reinforced polymers (GFRP), carbon fiber reinforced polymers (CFRP), and various thermoplastic matrix composites — are now the material of choice in sectors ranging from water treatment, chemical processing, and oil & gas to wind energy, civil infrastructure, and transportation.

The Asia-Pacific region remains the dominant market, accounting for over 45% of global FRP demand. India alone has seen a 12% year-on-year growth in FRP consumption, largely driven by government investments in water infrastructure, the expansion of the chemical manufacturing sector under the PLI (Production-Linked Incentive) scheme, and the booming renewable energy market requiring FRP structural components.

"Composites are no longer a niche material choice — they are rapidly becoming the baseline engineering standard for corrosive, outdoor, and high-load industrial applications." — C.V. Singh, Founder & Director, GPPL

Key Market Drivers

Several macro-economic and regulatory forces are simultaneously propelling FRP adoption:

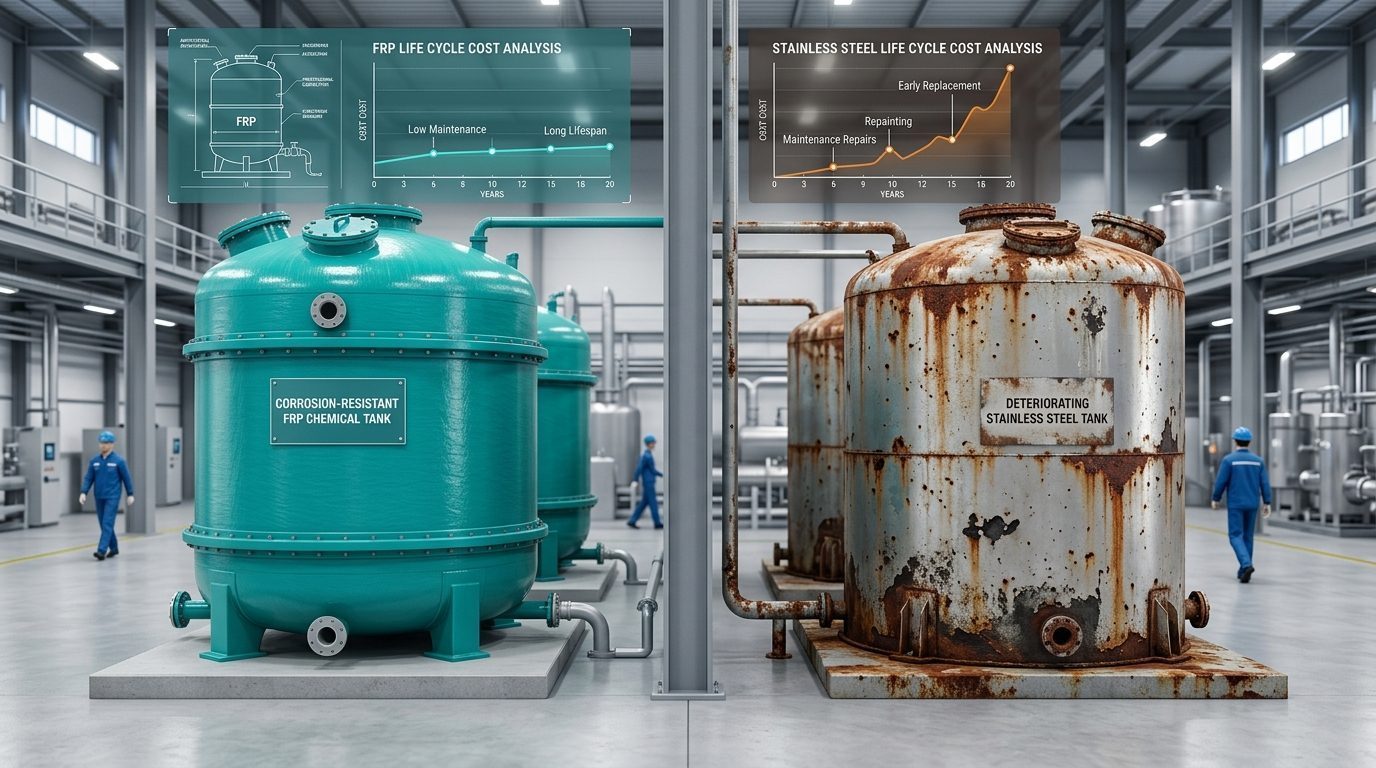

1. Corrosion-Driven Replacement Demand: The World Corrosion Organization estimates that global corrosion costs exceed USD 2.5 trillion annually — roughly 3.4% of global GDP. FRP's inherent chemical inertness makes it the most economical long-term solution for any structure in contact with corrosive media, replacing metal vessels and pipelines that require frequent maintenance and early replacement.

2. Environmental Regulations: Zero Liquid Discharge (ZLD) mandates in India, China, and Southeast Asia have led to mass construction of Effluent Treatment Plants (ETPs) — the majority of which specify FRP or dual-laminate thermoplastic vessels for their chemical resistance and low-maintenance profiles. The CPCB's revised ZLD guidelines (2024) have created a demand surge for chemical-resistant storage tanks and piping systems.

3. Infrastructure Investment Cycles: Government-backed infrastructure programs globally — including India's Jal Jeevan Mission (USD 50 billion in water infrastructure), the EU's Green Deal, and China's 14th Five-Year Plan — mandate the use of long-life, low-maintenance materials in water conveyance and treatment infrastructure. FRP pipes and tanks are the preferred specification.

4. Weight Reduction in Transport: The automotive and commercial vehicle sector is aggressively adopting FRP components to meet fuel efficiency and EV range targets. Lightweight FRP body panels, structural frames, and battery enclosures are now standard in next-generation EVs.

Regional Analysis

India: India's FRP market is expanding at one of the fastest rates globally. Key demand centers include the chemical corridors of Gujarat and Maharashtra, the pharmaceutical clusters of Hyderabad and Ahmedabad, and the growing water utility infrastructure in Tier-II cities. GPPL's position in the NCR industrial belt places it at the epicenter of this demand expansion.

China: China remains the world's largest producer and consumer of FRP composites. Its manufacturers are now moving up the value chain, exporting engineered composite products rather than raw materials. Competition from Chinese FRP manufacturers in the Indian market is intensifying, but quality differentiation — particularly ISO 9001 certifications and on-site engineering support — favors established Indian manufacturers.

Middle East & Southeast Asia: The oil and gas sector in the GCC countries and the expanding petrochemical industry in Southeast Asia represent fast-growing export markets for high-specification FRP storage and process equipment.

Future Outlook 2030

By 2030, the FRP market will be shaped by three transformational forces. First, recyclable thermoplastic composites will begin displacing thermoset FRP in non-critical applications, driven by ESG mandates that require end-of-life recyclability. Second, automated filament winding and pultrusion will bring manufacturing costs down by 20-30%, democratizing access to high-performance composite structures. Third, smart composites — FRP structures embedded with IoT sensors for real-time structural health monitoring — will emerge as the standard for critical infrastructure applications.

For procurement teams and plant engineers evaluating long-term capex investments, the message is clear: the transition to FRP composites is not a future consideration, but a present-day commercial imperative. The material that was once a premium specialty is rapidly becoming the lowest total-cost-of-ownership option across virtually every industrial application class.

Conclusion

The global FRP market's growth trajectory signals a fundamental, multi-decade shift in industrial material engineering. For Indian chemical manufacturers, water utilities, and plant operators, domestic manufacturers like GPPL — who combine 30+ years of engineering experience with full ISO 9001:2015 certification — offer the ideal combination of technical expertise and responsive, on-site support that global competitors cannot match. As the market matures, the competitive advantage will belong to those who adopted FRP early, understanding not just the material, but the engineering discipline required to specify and maintain it correctly.